With 2024 fully behind us, it’s a good time to celebrate our winning calls from last year while also reviewing some mistakes to learn from them and improve our process. The good news is we got more right than wrong last year, but there were some misses. Some course corrections helped. Perhaps the most impactful decision we made was to recommend investors stay fully invested in equities at benchmark levels throughout the entire year despite expecting a stock market pullback around Election Day.

What We Got Right and Wrong in Equities

Staying Fully Invested. Let’s start with our most important call — our tactical recommendation on equities. While staying neutral all year may seem like a miss (of course, an overweight would’ve been better), a downgrade was tempting given the risks. Recall back in late 2023 how widespread recession fears were. Wall Street price targets, including ours, called for single digit returns. A downgrade was tempting given the magnitude of the gains, narrow leadership, and rich valuations.

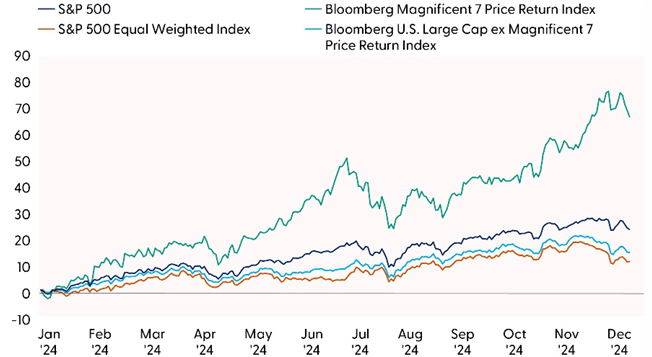

Despite all the concentration risk headlines surrounding mega-cap tech stocks, staying fully invested in U.S. equity markets was the correct call last year. The outperformance and amplified attention of the Magnificent Seven names — Alphabet (GOOG/L), Amazon (AMZN), Apple (AAPL), Meta (META), Microsoft (MSFT), NVIDIA (NVDA), and Tesla (TSLA) — masked relatively broad participation in the S&P 500’s rally last year. Throughout 2024, an average of 73% of S&P 500 stocks closed above their 200-day moving average (dma), marking the sixth-best year of breadth since the data series began in 1991.

As we know now, stocks defied the skeptics and kept going higher almost without interruption in 2024. The maximum S&P 500 drawdown into the August low reached 8.5%. With the benefit of hindsight, this would have been an opportune time to dial up equity market risk to overweight, a profitable trade we contemplated but ultimately missed. The swift recovery into September caught us off guard, but fortunately, and despite some technical damage and political uncertainty, we at least did not turn negative on equity markets.

Mega Caps Did a Lot of Heavy Lifting Last Year

Source: LPL Research, Bloomberg, 01/02/25

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

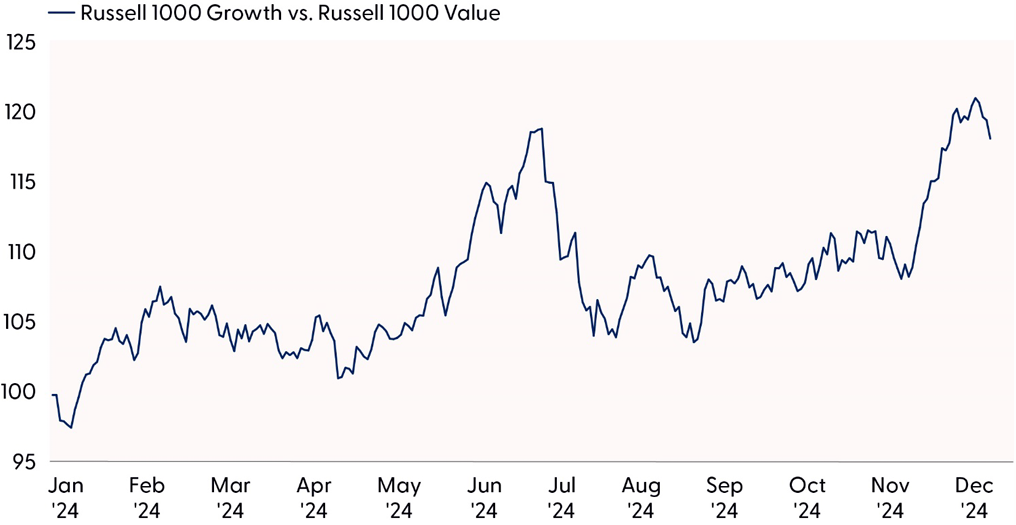

Growth Over Value. This call, which our Strategic and Tactical Asset Allocation Committee (STAAC) maintained all year, was a big winner, with the growth style outperforming its value counterpart by 19 percentage points (33% to 19%) for the year, based on the Russell 1000 style indexes. With prevalent calls for a rotation into more attractively valued value stocks, high expectations for artificial intelligence (AI) investment, and our use of technical analysis kept us in the growth trade throughout 2024.

Dominant Performance by Growth Stocks in 2024 Fueled by the Magnificent Seven

Growth beat value by more than 18 percentage points in 2024

Source: LPL Research, Bloomberg, 01/02/25

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Overweight Communication Services, Underweight Real Estate. Two of our sector calls last year were spot on, as the STAAC maintained an overweight to communication services and an underweight to real estate throughout the entire year. Communication services was the year’s top performer with its 40.2% return, while real estate gained just 5.2% for the year, topping only healthcare (+2.5%) and materials (unchanged). Our preference for faster-growing sectors leveraged to AI, election ad spending, and a resilient economy with relatively less interest rate sensitivity underpinned our preference for communication services and cautious stance toward real estate.

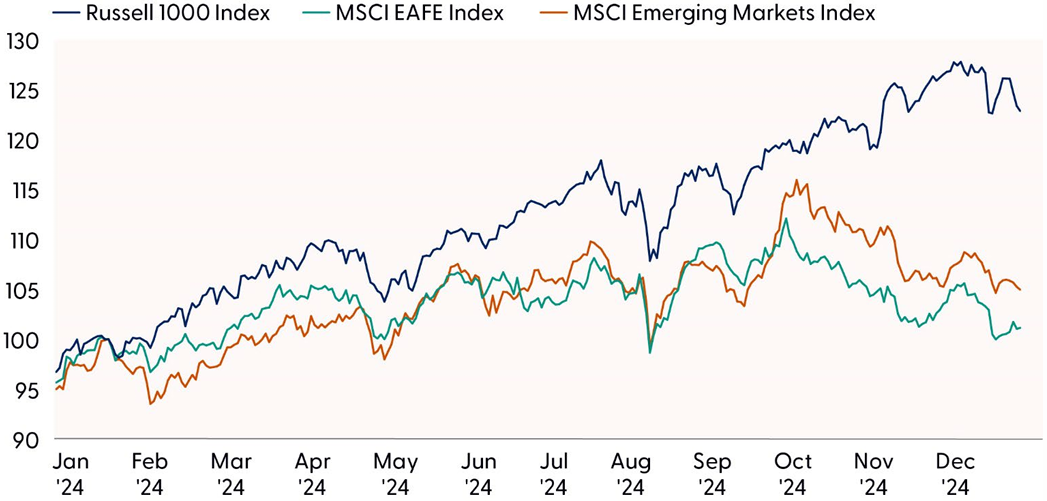

Favoring U.S. Over EM. Emerging market (EM) equities dramatically underperformed as the MSCI EM Index returned 8% last year. Inferior economic and earnings growth and a strong U.S. dollar (up over 7% for the year) weighed on EM for much of the year, while tariff and trade worries offset the effects of more stimulus in China late in the year. South Korea (-23.2%) was a particularly large drag on EM performance. LPL Research’s asset allocation committee’s skepticism toward the Chinese economy and our AI innovation advantage also played into the U.S. preference.

U.S. Equities Outperformed International and EM from Start to Finish in 2024

U.S. equities soundly outpaced primary international and EM benchmarks in 2024

Source: LPL Research, Bloomberg, 01/02/25

Disclosures: All indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

S&P 500 Price Target Was Too Low. The biggest miss last year for LPL Research was the low S&P 500 year-end fair value target. After starting the year with 4,900 at the high end of the range, LPL Research raised it to 5,500 in the fall and the index galloped well beyond that target. We did not anticipate so much price-to-earnings (P/E) multiple expansion given higher interest rates. As it turned out, the macroeconomic and profits outlook was strong enough to support a P/E near 22 times forward earnings estimates, not the anticipated 19–20.

Energy Recommendation Was Another Miss. The overweight recommendation on the energy sector from the start of 2024 through August was a loser as the sector underperformed by about 8% during that time. The good news is the team smartly downgraded the sector in August and again in September before another 10 percentage points of additional underperformance through year-end. The team put too much emphasis on better capital allocation decisions, more shareholder-friendly management teams, and geopolitical threats, and not enough on the drag on U.S. oil prices from strong production.

What We Got Right and Wrong in Fixed Income

Disappointing Year for Fixed Income. It was arguably a disappointing year for high-quality fixed income markets based on Bloomberg Aggregate Bond Index performance. Investors should reasonably expect to receive coupon income each year (which they did), but that was largely offset by the move higher in interest rates. It was a volatile year for interest rates, with the 10-year trading between 3.62% and 4.71% and the 2-year between 3.50% and 5.04%. Ever-evolving Federal Reserve (Fed) rate cut expectations were the primary drivers of volatility, while concerns about ongoing fiscal budget deficits and Treasury supply added to the elevated rate moves.

The volatile rate environment allowed us to close out our overweight fixed income recommendation/allocation in early October near the lows in interest rates of the year, and our neutral duration recommendation since then hasn’t hurt us as interest rates continued to climb through year-end.

But the “winning” call for fixed income was to strongly overweight the preferred security asset class, which turned out to be the best-performing major asset class within fixed income in 2024. Preferreds are generally issued by financial institutions, and after the regional banking concerns that took place in March 2023, we initiated a position in portfolios and recommended a strong overweight. Yields and spreads, we felt, provided enough compensation to invest in an area that was likely going to experience volatility and that broadly came to fruition. The preferred index (ICE BofA US All Capital Securities) was up nearly 10% for the year (after being up 9% in 2023 as well). We recently downgraded our recommendation/allocation to a modest overweight after the strong run in preferreds — we still like the sector, but not as much as we did a year ago.

Credit Was a Miss. In terms of misses last year, we underestimated the ongoing resilience in corporate credit markets — both investment grade and high yield. Our economic call for most of 2024 was for the U.S. economy to slow down. That never really happened, so positive economic conditions allowed credit markets to remain expensive. While our recommendation to invest in the short-to-intermediate parts of the investment grade corporate credit space worked (that part of the credit curve outperformed the broad maturity index by nearly 3% in 2024), our decision to underweight the sector broadly was wrong (although we used the underweight to fund the preferred allocation).

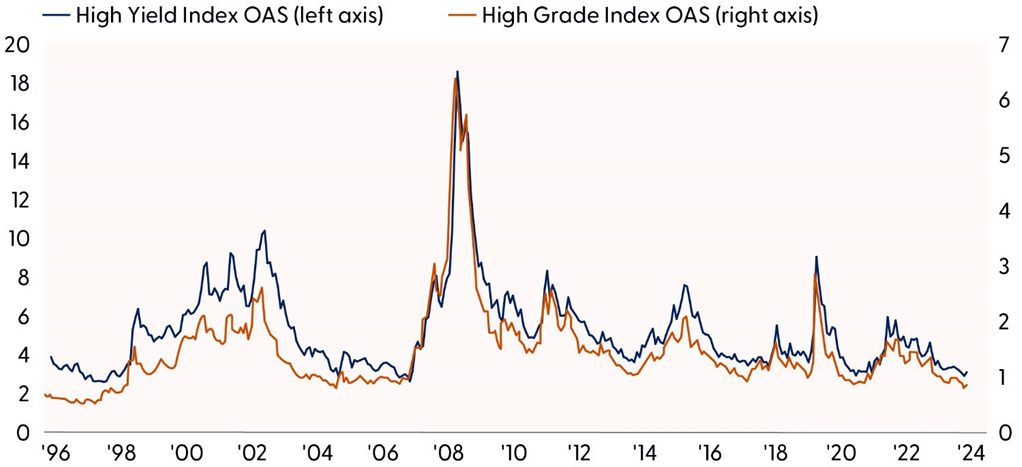

Not Enough High-Yield. The decision to not invest in high-yield bonds was also a miss. High-yield bonds (and loans) were up over 8% on the year and spreads remained relatively contained. We were waiting for spreads to widen to change our recommendation, but that never happened. As highlighted in the chart below, spreads (for both high yield and investment grade) remain at or near secular tights. The last time investment grade spreads were this low was back in 1997 and in 2007 for high yield. Going into 2025, our views on the corporate credit market remain the same — we think the markets are too expensive and aren’t really interested in either market. But unless/until economic conditions deteriorate, spreads will likely stay at these tight levels.

Corporate Credit Markets Are Resilient but Expensive

Credit spreads remain near/at secular tights

Source: LPL Research, Bloomberg, 01/02/25

Disclosures: Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Conclusion

There you have it, our hits and misses from 2024. We’re pleased to report more hits than misses last year and we’re hard at work to try to deliver more of the same in 2025. On behalf of the LPL Research team, thanks for your interest in our content and your trust in LPL Research as your investment partner.

Asset Allocation Insights

As 2025 begins, LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities, with a preference for the U.S. over international and emerging markets, a slight tilt toward growth, and benchmark-like exposure across the market capitalization spectrum. The Committee recommends benchmark-level fixed income exposure, with an emphasis on intermediate maturities, and an allocation to preferred securities.

As discussed in our Outlook 2025: Pragmatic Optimism and previous Weekly Market Commentary, we expect stocks to move modestly higher in 2025 while acknowledging reasonable upside and downside scenarios. We cannot rule out the possibility of short-term weakness as sentiment remains stretched and a lot of good news is priced into markets. Upside support could come from economic growth, a supportive Fed, strong corporate profits, and supportive policies from the Trump administration. The most likely downside scenarios involve re-accelerating inflation, higher interest rates, and geopolitical threats that do economic harm. If inflation re-accelerates, equities may need to readjust to what could be a slower and shallower Fed rate-cutting cycle than markets are currently pricing in.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy

All investing involves risk, including possible loss of principal.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet or Bloomberg.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

For public use.

Member FINRA/SIPC.

RES-0002683-1224 Tracking #677754 | #677755 (Exp. 01/26)