The Federal Reserve (Fed) is moving more cautiously in adjusting policy, and markets might have a hard time resetting expectations. Throughout the latest press conference with Fed Chair Jerome Powell, equity markets declined as investors were befuddled with the large upward revision to 2025 inflation forecasts; despite disappointing inflation projections, the “vibecession” is over as businesses and consumers have become more optimistic. We highlight pent-up demand for capital investment that could provide support in the new year.

Key Takeaways

- The Fed will not cut rates as much as initially expected. The “extent and timing” of policy adjustments is code that the Fed is unsure about the future path of interest rates given the strength of the economy.

- The biggest surprise was the upward revision to inflation next year. Fed officials project a 2.5% inflation rate by the end of 2025, up from the 2.1% forecast in September and most likely reflecting uncertainty from potential trade wars.

- The Fed says it will reduce the rate it pays lenders using the overnight reverse repurchase facility by 30 basis points, effectively lowering the rate by five basis points relative to the federal funds target range.

- A hawkish Fed amid more dovish global central banks will provide upside for the U.S. dollar in the coming year.

- If the job market cools, consumer spending will likely moderate in 2025, while pent-up demand for capital investment could provide support.

The Hawkish Cut

Not surprisingly, investors got what they expected. The Federal Open Market Committee (FOMC) cut the target rate by 0.25% to 4.25–4.50% at its December 18 meeting. Further, the FOMC signaled fewer cuts in 2025 and acknowledged the potential for stickier inflation and increased policy uncertainty.

Moreover, Cleveland Fed President Beth Hammack dissented in favor of a hold, as inflation has been moving sideways for a while. A slower projection of inflation returning to target, forecasts for fewer cuts to come, and Powell’s characterization of rates as “significantly closer to neutral” were seemingly more hawkish than markets expected.

While the bond market had largely priced in the prospects of fewer cuts, the potential for stickier inflation and policy uncertainty pushed Treasury yields higher, with the two- and 10-year rising notably last Wednesday following the cut.

The revised outlook telegraphed to markets that the Fed intends to cut rates two times next year instead of four as projected just a few months ago.

With policy uncertainty still elevated, particularly as it relates to the economic impact of the incoming Trump 2.0 administration, we continue to think a neutral duration (interest rate sensitivity) for fixed income portfolios versus benchmarks is warranted. And for those investors interested in income opportunities, we think the front end out to the belly of both the interest rate and credit curves remains attractive.

Upending Equilibrium

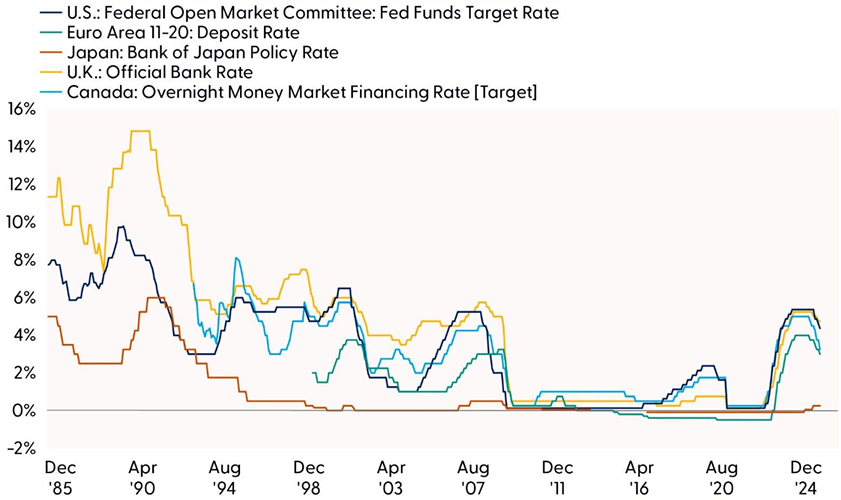

As depicted in the “Global Bankers Never More Synchronous” chart, global central banks have never been more synchronous than this past year. Of course, that’s excluding the Bank of Japan with its incredibly accommodative policy and subsequent weak-performing currency.

Global Bankers Never More Synchronous

A Fed Recalibration Could Upend Equilibrium

Source: LPL Research, Bank of Canada, Bank of England, Bank of Japan, European Central Bank, Federal Reserve, 12/23/24

So, one thing markets will have to deal with in 2025 is the potential for the Fed to pause policy adjustments while other major global policy rates continue to step downward. November inflation was more benign than expected, but the stickiness of some categories supports the Fed’s hesitancy to materially lower rates next year. Despite the softer monthly pace, headline annual inflation rose to 2.4% from 2.3% last month due to year-over-year base effects. Annual core inflation was unchanged at 2.8%, higher than the Fed’s 2% target and the main reason the Fed will not likely cut rates as much as they initially projected. Inflation is supported by a robust economy, which continues to grow from strong consumer demand as income growth and the wealth effect from higher portfolio values give consumers the capacity to spend.

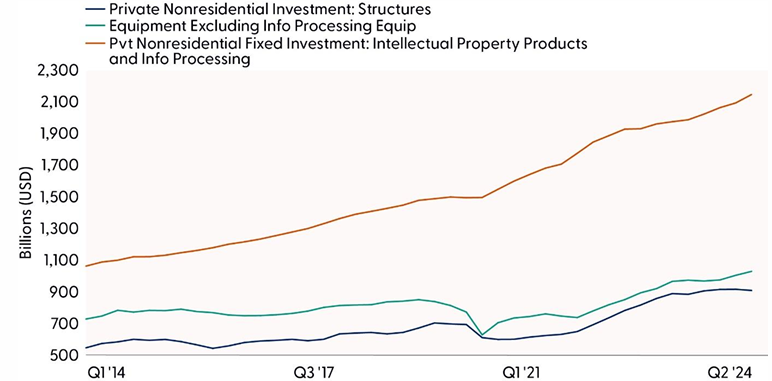

Businesses Have a Big Appetite for R&D

Many businesses admitted they temporarily delayed business fixed investments preceding the presidential election and planned to wait until after results were finalized and the policy outlook was a bit clearer. As we have seen, policy tailwinds supported the business and consumer outlook.

Businesses Invested Heavily in Intellectual Property

Pandemic Accelerated Appetite for R&D

Source: LPL Research, Bureau of Economic Analysis, 12/23/24

We think the strong trajectory for capital spending, especially for intellectual property and information processing equipment, will continue. Businesses are putting a larger share of their spending on research and development (R&D) as the race for improved artificial intelligence continues (“Businesses Invested Heavily in Intellectual Property” chart). Surveys suggest businesses have pent-up demand now that we are past the elections. Construction spending for healthcare, power, communication, and other structures is poised to increase, and shipments of capital goods are below current run rates, corroborating business owners’ comments about delaying, but not canceling capital expenditures (CAPEX).

In addition to the pent-up demand for CAPEX, a pro-business tax and regulatory plan could also increase business spending while providing a modest tailwind to the economy. On balance, this should be enough of a boost to growth to offset some ease in consumer spending and set us up for stable, but unspectacular gross domestic product (GDP) growth in 2025.

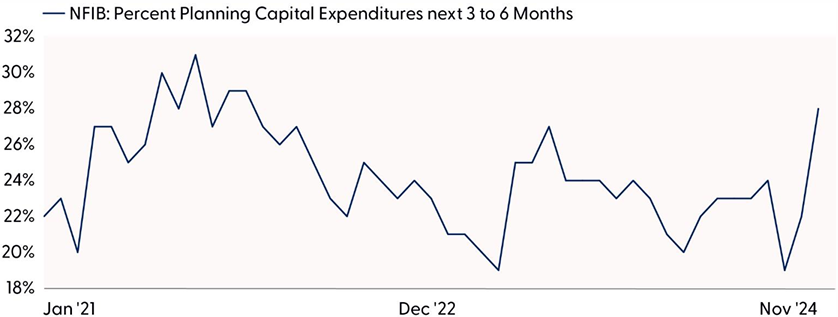

Businesses Have a New Vibe

The percentage of businesses planning to increase capital spending in the next several months rose to the highest since mid-2021. No more “vibecession” within the corporate sector and probably not in the consumer sector either, as households feel more optimistic about their financial situation.1

NFIB Monthly Survey Spiked After Election

Largest Percentage Since Mid-2021

Source: LPL Research, Natl Federation of Independent Business, 12/23/24

Summary

The recent FOMC meeting brought back some unwanted clouds of uncertainty over monetary policy next year. At a minimum, market expectations have shifted toward a shallower- and slower-than-anticipated rate-cutting cycle. However, the Fed cannot take all the blame for the selling pressure, as a reality check from overbought conditions, deteriorating market breadth, and rising rates appeared overdue. Upside risks remain for Treasury yields and the U.S. dollar, creating potential headwinds for stocks. Based on this backdrop and the recent technical damage to the broader market, including a notable deterioration in market breadth over the last few weeks, we recommend waiting for support to be established and for momentum to improve before stepping up to buy this dip.

Asset Allocation Insights

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities, with a preference for the U.S., a slight tilt toward growth, and benchmark-like exposure across the market capitalization spectrum. However, we do not rule out the possibility of short-term weakness as sentiment remains stretched and a lot of good news is priced into markets even as interest rates are pushing higher and geopolitical threats escalate. Equities may also need to readjust to what could be a slower and shallower Fed rate-cutting cycle than markets are currently pricing in, although December seasonality is favorable.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet or Bloomberg.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

For public use.

Member FINRA/SIPC.

RES-0002562-1124 Tracking #674313 | #674447 (Exp. 12/25)