The clouds of uncertainty parted last week as former President Donald Trump decisively won the U.S. election, making him the second U.S. president to win non-consecutive terms (Grover Cleveland was the first to do it back in 1892). Investors welcomed the news with renewed risk appetite, bidding the S&P 500 to its 50th record high of the year on Friday. Trump’s proposed economic policies, including deregulation, a likely extension of the 2017 tax cuts, a possible corporate tax rate cut, and proposed tax exemptions on tips, social security, and overtime pay helped underpin buyer enthusiasm. The immediate de-risking of when the election will be decided was another big factor behind the post Election Day rally.

Stocks were not the only asset class on the move last week, as Treasury yields and the dollar also advanced. Growth expectations re-rated higher as the market priced in more economic-friendly policy proposals. However, the improving growth outlook was accompanied by concerns over the deficit and rising inflation, especially with Trump’s proposed tariff policies. Herein, we discuss these themes and other major election takeaways for investors.

The Bull Market Survives Election Day

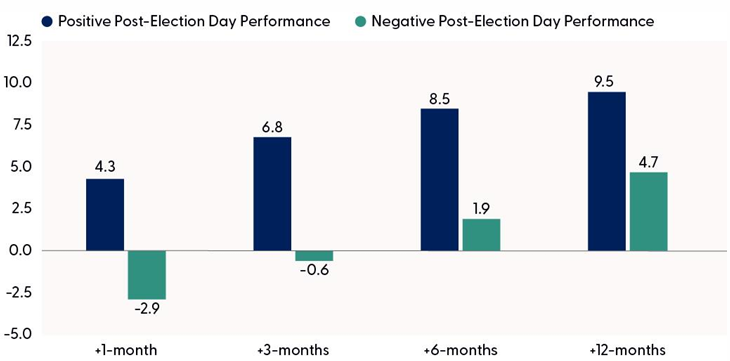

While we are only a few days removed from Election Day, we feel comfortable stating the bull market not only survived one of this year’s biggest event risks but thrived in the face of uncertainty. The S&P 500 rallied 2.5% on Wednesday, November 6, with most of the buying done overnight as Trump tallied up electoral votes. By the opening bell, the index gapped higher by over 1% and didn’t look back, closing at a fresh record high of 5,929 on Wednesday. This marked the best post-Election Day performance for the broader market on record. Given investors’ exceptionally warm reception of the election outcome, we analyzed previous elections to identify how positive or negative post-Election Day performance correlates to future returns.

As the chart below highlights, positive performance after Election Day tends to be a good sign for future returns. Of the nine other post-Election Day advances since 1928, the index gained 4.3% over the following month, with only one period producing a negative return (1936 was the last time the market was lower one month after a positive post-Election Day performance). Longer-term, three-, six-, and 12-month returns averaged 6.8%, 8.5%, and 9.5%, respectively. For comparison, when the market is lower after Election Day, three-, six-, and 12-month returns have averaged -0.6%, 1.9%, and 4.7%, respectively.

Post-Election Day S&P 500 Performance Has Been a Good Sign for Future Returns

Source: LPL Research, Bloomberg 11/07/24

Past performance is no guarantee of future results. The modern design of the S&P 500 stock index was first launched in 1957.

Performance back to 1950 incorporates the performance of the predecessor index, the S&P 90

Small Cap Enthusiasm May Be Overdone

At the risk of throwing some rain on the post-election parade, we believe the enthusiasm for small cap stocks may be getting somewhat overdone for two primary reasons. First, one key element of the small cap trade is lower taxes under Trump 2.0. But given the federal budget situation, when the horse-trading begins next year in Washington, D.C., we expect some pressure from centrists and deficit hawks, even under a Republican sweep of Congress (likely, but not assured as votes are still being counted), to keep the corporate rate where it is at 21%. Efforts to provide tax incentives for domestic production could work, but the effects could be minimal. And that’s putting aside the fact that the expiration of the Tax Cuts and Jobs Act of 2017 is still more than a year away.

Domestic production is another reason for the bullishness on small caps. Another element of the bull case is that smaller companies are more U.S.-focused and less impacted by tariffs. That may be true, but for the profitable companies that make up the S&P Small Cap 600 Index, we estimate that over one-third of profits are generated outside the U.S., perhaps less than five points lower than international earnings within the S&P 500. In fact, a recent study by our friends at Ned Davis Research indicated the difference in the international profit mix between the S&P 500 and S&P 600 for companies that have reported third-quarter results so far is just 1%!

Rising rates are another risk factor to consider, as smaller companies tend to be more interest rate sensitive due to a greater reliance on bank lending. Though LPL Research expects limited additional upside to long term interest rates, the lack of fiscal discipline is a concern.

Our technical analysis work also suggests some caution inchasing the small cap rally. As highlighted below, the small-cap-centered Russell 2000 Index still faces key resistance off the 2021 highs at 2,459. And while momentum indicators have recently turned bullish, overbought conditions have subsequently developed, pointing to near-term risk for a pullback — overbought conditions paired with overhead resistance is a recipe for some profit-taking.

Despite stints of excitement surrounding small caps, they have underperformed large caps for the last several years. This trend is apparent in the Russell 2000 vs. S&P 500 ratio chart in the second panel of the chart below. Technically, until this trend is reversed, momentum remains in favor of large cap leadership ahead. Finally, we caution drawing any major performance parallels to the 2016 election, as small caps were decisively outperforming large caps that year, well before Election Day.

Small Caps Rally, but Can They Finally Lead?

Source: LPL Research, Bloomberg 11/07/24

Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly

On the positive side, de-regulation and a steeper yield curve is bullish for the banks, which make up a greater portion of the small cap indexes. And small cap valuations remain supportive of smaller-cap companies. Bottom line, LPL Research’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its recommendation for balance across market cap, including benchmark-level exposure to large, mid, and small cap stocks.

Interest Rates React

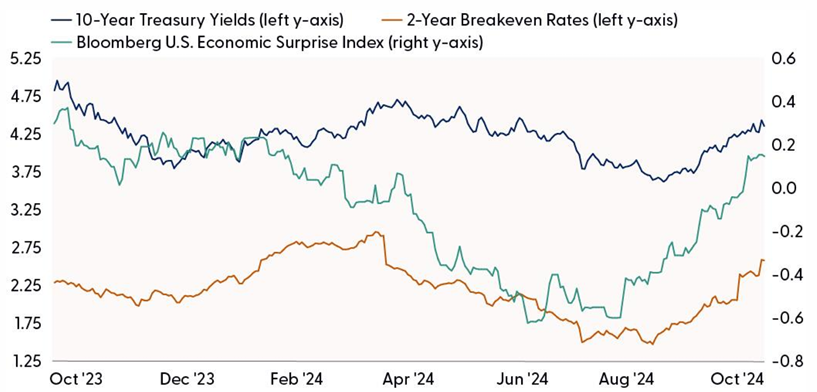

For the rates markets, despite the recent run-up in Treasury yields, there is still room for yields to move higher — for both good and bad reasons. Since the recent lows back on September 16, the 10-year Treasury yield is higher by nearly 0.70%. Markets are forward-looking and tend to adjust based upon expectations. However, given the unpredictable nature of economic data, consensus expectations may be wrong at times, which causes another market adjustment.

So, after hovering around the lowest levels since 2015, the Bloomberg U.S. Economic Surprise Index (the light blue line in the chart below) has been trending higher lately, reflecting economic data that has been, in general, better than consensus expectations. And since Treasury yields have fallen alongside negative economic surprises, it isn’t surprising that yields are now moving higher given better economic data and, as a result, fewer Federal Reserve (Fed) rate cut expectations. While that’s generally negative for Treasury yields, better economic data means the economy still isn’t showing signs of slowing. Even Fed Chair Jerome Powell addressed the recent jump in rates during the post-Federal Open Market Committee (FOMC) presser, stating, “The moves are not principally about higher inflation expectations; they’re really about a sense of more likelihood of stronger growth, and perhaps less in the way of downside risks.”

Another reason yields have moved higher is that the bond market isn’t fully convinced the inflation genie is back in the bottle. The risk for the bond market is a Fed that cuts too aggressively into a still-growing economy, which would then potentially rekindle inflation concerns. Moreover, as it relates to the Trump presidency, there is a concern that deficit spending (which would have likely happened under a Harris presidency as well) and tariffs could help growth but also keep inflationary pressures elevated. Of that recent move higher in the 10-year Treasury yield, roughly 40% of the move can be attributed to inflation concerns.

Treasury Yields Advance Amid Higher Growth and Inflation Expectations

Source: LPL Research, Bloomberg 11/07/24

Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly

Better economic growth data, perhaps a too-dovish Fed, and more policy details from the Trump administration could push Treasury yields higher. It will likely take negative economic surprises for yields to fall meaningfully from current levels. Next month’s jobs report (December 7) will be an important data point to watch. Given the weather-related distortions in the previous payroll report, the December 7 release may turn out to be stronger than expected, bringing a heightened level of confusion for investors as the government counters play catch-up from last month. Further complicating things, upcoming inflation data could come in on the high side, pulling up the year-over-year metrics. We do not think a second wave of inflation is likely, but investors should expect a head-fake in the initial data.

As the Fed manages the balance of risks, investors should revisit capital market assumptions as they prepare for 2025. We should get a better understanding of the minds of Fed policymakers when they publish an updated Summary of Economic Projections at the December policy meeting, and we should not be surprised if projected policy rates at the end of 2025 are raised higher.

Summary

As Americans, politics are part of our DNA, and despite all our disagreements, or the election outcome, we have moved forward with optimism and resilience since 1776. And while a Trump victory may or may not have been what you were hoping for, we can at least breathe a sigh of relief the election is over and embrace a world of no more political advertisements! For investors, policy does matter, especially when it relates to tax and trade, but as we have stressed, earnings, inflation, interest rates, and other macro forces are really the key drivers of longer-term performance.

Asset Allocation Insights

This bull market continues to enjoy solid momentum, supported by steady economic growth, moderating inflation, solidly rising corporate profits, clarity around the policy road map post-election, and favorable seasonality. At the same time, valuations are elevated, interest rate risk is rising, geopolitical threats remain, and we are probably due for a pullback after such a strong year-to-date rally.

LPL’s STAAC continues to recommend investors stay fully invested at their targets for both equities and fixed income from a tactical asset allocation perspective — with potentially a small alternative investments position, funded from cash, to help mitigate potential volatility for appropriate investors. The STAAC maintains a slight preference for growth over value, recommends keeping allocations across market caps generally in line with benchmarks, favors U.S. equities over their international and emerging markets counterparts, and recommends an up-in-quality approach to fixed income.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet or Bloomberg.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

For public use.

Member FINRA/SIPC.

RES-0002171-1024W Tracking #656134 (Exp. 11/25)